-

6 Publicações

-

0 fotos

-

0 Vídeos

-

Male

-

Seguido por 8 pessoas

Pesquisar

Atualizações Recentes

-

Benefits of a Colocation Data Center

A colocation data center regularly denoted as a ‘colo,’ is any big data center capacity that rents out blank space to third parties for setting up their servers or other network devices. This is a very commonly used service that is utilized by companies that may not have the required space or facilities to maintain their data center but still needs to utilize all the advantages.

What is Colocation?

The term colocation states to numerous features of this kind of data center. First, the term positions the fact that servers and other gears from several different businesses are ‘co-located’ in one huge data center. The computer hardware is generally possessed by the companies themselves and maintained by the data center operators.

It also states the idea that a business can have its gear situated in various places. They may have servers, for instance, in four or five diverse colocation data centers. This is vital for businesses that have huge geographic footprints, and they need to ensure their computer systems are situated near their bodily offices.

Advantages of a Colocation Data Center

For businesses, or even people, who need to utilize colocation data center services, there are numerous great aids that they can enjoy.

Lower Prices – On the basis of the price of a colocation data center with the choice of building your own facility, it is a clear choice. Unless your machine needs a vast amount of space, the prices will be far inferior when using a colocation choice.

Less Technical Staff – You do not require to be concerned about things like managing power, running cables, installing equipment, or any number of other mechanical processes. In several cases, the colocation data center will even be allowed to replace mechanisms or perform other tasks as demanded. This means you don’t require to have a huge IT staff working to handle this stuff.

Exceptional Dependability – Colocation data centers are characteristically manufactured with the uppermost specifications for redundancy. This comprises outstanding physical security, backup power generators, numerous network connections via multiple telcos, and much more.

Geographic Location – You have the option to choose the size of your data center so that it is close to your operators.

Foreseeable Expenses – The prices allied with a colocation data center will be very expectable. You can characteristically sign contracts that last one or more years, so you know precisely how to budget your IT requirements.

Simple Scalability – When your company is rising, you can rapidly have new servers or other gear added to the facility. When you have your machine in a compact local data center or server closet, it can be greatly more problematic to scale.

Hence, Colocation enables data storage extension to fit the requirements of a business. Businesses can raise their networks without being need to buy more machines or construct space. When your business grows, your IT infrastructure can develop to fulfill your requirements rapidly and with less expenditure, such factors are driving the data Center Colocation industry.

Read More: https://www.psmarketresearch.com/market-analysis/data-center-colocation-marketBenefits of a Colocation Data Center A colocation data center regularly denoted as a ‘colo,’ is any big data center capacity that rents out blank space to third parties for setting up their servers or other network devices. This is a very commonly used service that is utilized by companies that may not have the required space or facilities to maintain their data center but still needs to utilize all the advantages. What is Colocation? The term colocation states to numerous features of this kind of data center. First, the term positions the fact that servers and other gears from several different businesses are ‘co-located’ in one huge data center. The computer hardware is generally possessed by the companies themselves and maintained by the data center operators. It also states the idea that a business can have its gear situated in various places. They may have servers, for instance, in four or five diverse colocation data centers. This is vital for businesses that have huge geographic footprints, and they need to ensure their computer systems are situated near their bodily offices. Advantages of a Colocation Data Center For businesses, or even people, who need to utilize colocation data center services, there are numerous great aids that they can enjoy. Lower Prices – On the basis of the price of a colocation data center with the choice of building your own facility, it is a clear choice. Unless your machine needs a vast amount of space, the prices will be far inferior when using a colocation choice. Less Technical Staff – You do not require to be concerned about things like managing power, running cables, installing equipment, or any number of other mechanical processes. In several cases, the colocation data center will even be allowed to replace mechanisms or perform other tasks as demanded. This means you don’t require to have a huge IT staff working to handle this stuff. Exceptional Dependability – Colocation data centers are characteristically manufactured with the uppermost specifications for redundancy. This comprises outstanding physical security, backup power generators, numerous network connections via multiple telcos, and much more. Geographic Location – You have the option to choose the size of your data center so that it is close to your operators. Foreseeable Expenses – The prices allied with a colocation data center will be very expectable. You can characteristically sign contracts that last one or more years, so you know precisely how to budget your IT requirements. Simple Scalability – When your company is rising, you can rapidly have new servers or other gear added to the facility. When you have your machine in a compact local data center or server closet, it can be greatly more problematic to scale. Hence, Colocation enables data storage extension to fit the requirements of a business. Businesses can raise their networks without being need to buy more machines or construct space. When your business grows, your IT infrastructure can develop to fulfill your requirements rapidly and with less expenditure, such factors are driving the data Center Colocation industry. Read More: https://www.psmarketresearch.com/market-analysis/data-center-colocation-market0 Comentários 0 Compartilhamentos 5K Visualizações 0 Anterior -

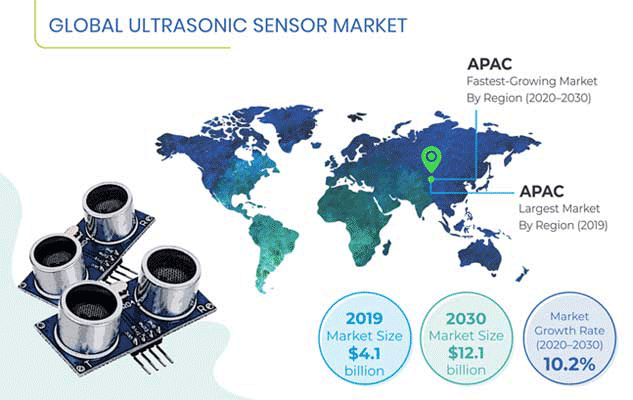

Explosive Growth Expected in Asia-Pacific Ultrasonic Sensor Market in Future

The global ultrasonic sensor market generated a revenue of $4.1 billion in 2019 and is predicted to reach a value of $12.1 billion by 2030. According to the forecast of the market research firm, P&S Intelligence, the market will progress at a CAGR of 10.2% between 2020 and 2030. The surging usage of ultrasonic sensors in automobiles and the growing requirement for these sensors in the manufacturing industry are the two main factors driving the progress of the market.

In manufacturing industries, ultrasonic sensors are extensively used for several applications such as the diameter measurement of roll, loop control, distance measurement, height measurement, and tank water level measurement. Furthermore, with the rapid surge in industrial production in the developing countries, the requirement for ultrasonic sensors, especially in level measurement applications, is soaring quickly. For example, as per reports published in September 2019, in Turkey, the industrial production increased by nearly 3.4% year-on-year.

The burgeoning usage of these sensors in automobiles is another important factor fueling the growth of the market. Ultrasonic sensors are heavily used in vehicles in several applications such as park assistant systems, level sensing in fuel tanks, and object identification and detection. Due to the ballooning automobile manufacturing, especially in the emerging economies such as Thailand, Indonesia, and China, the sales of ultrasonic sensors are rising sharply all over the globe.

Besides the aforementioned factors, the rising requirement for industrial automation is predicted to create huge growth opportunities for the players operating in the ultrasonic sensor market in the coming years. The implementation of the Industry 4.0 program in the manufacturing industry is predicted to boost the requirement for automation in several industrial processes in the future years. Furthermore, manufacturers are rapidly incorporating automation in various manufacturing operations for augmenting the productivity.

Depending on end user, the ultrasonic sensor market is divided into automotive, healthcare, industrial, agriculture, and food & beverage categories. Out of these, the automotive category is predicted to demonstrate the fastest growth in the market in the coming years. This is credited to the rising requirement for ultrasonic sensors for detecting obstacles in self-driving vehicles. These sensors are used in self-driving vehicles for various distance measurement applications. This causes a sharp reduction in the incidence of road accidents.

Geographically, the ultrasonic sensor market recorded the highest growth in the Asia-Pacific (APAC) region during the last few years and is also predicted to demonstrate the fastest growth in this region in the coming years. The main factors propelling the advancement of the market are the soaring automobile manufacturing and the booming industrial manufacturing sector, primarily in India, China, and Thailand. Additionally, the rising requirement for smart farming equipment will propel the market growth in the region in the future.

Hence, it can be said with confidence that the market will register huge growth around the world in the upcoming years, mainly because of the mushrooming usage of ultrasonic sensors in vehicles and various manufacturing operations.

Read More: https://www.psmarketresearch.com/market-analysis/ultrasonic-sensor-marketExplosive Growth Expected in Asia-Pacific Ultrasonic Sensor Market in Future The global ultrasonic sensor market generated a revenue of $4.1 billion in 2019 and is predicted to reach a value of $12.1 billion by 2030. According to the forecast of the market research firm, P&S Intelligence, the market will progress at a CAGR of 10.2% between 2020 and 2030. The surging usage of ultrasonic sensors in automobiles and the growing requirement for these sensors in the manufacturing industry are the two main factors driving the progress of the market. In manufacturing industries, ultrasonic sensors are extensively used for several applications such as the diameter measurement of roll, loop control, distance measurement, height measurement, and tank water level measurement. Furthermore, with the rapid surge in industrial production in the developing countries, the requirement for ultrasonic sensors, especially in level measurement applications, is soaring quickly. For example, as per reports published in September 2019, in Turkey, the industrial production increased by nearly 3.4% year-on-year. The burgeoning usage of these sensors in automobiles is another important factor fueling the growth of the market. Ultrasonic sensors are heavily used in vehicles in several applications such as park assistant systems, level sensing in fuel tanks, and object identification and detection. Due to the ballooning automobile manufacturing, especially in the emerging economies such as Thailand, Indonesia, and China, the sales of ultrasonic sensors are rising sharply all over the globe. Besides the aforementioned factors, the rising requirement for industrial automation is predicted to create huge growth opportunities for the players operating in the ultrasonic sensor market in the coming years. The implementation of the Industry 4.0 program in the manufacturing industry is predicted to boost the requirement for automation in several industrial processes in the future years. Furthermore, manufacturers are rapidly incorporating automation in various manufacturing operations for augmenting the productivity. Depending on end user, the ultrasonic sensor market is divided into automotive, healthcare, industrial, agriculture, and food & beverage categories. Out of these, the automotive category is predicted to demonstrate the fastest growth in the market in the coming years. This is credited to the rising requirement for ultrasonic sensors for detecting obstacles in self-driving vehicles. These sensors are used in self-driving vehicles for various distance measurement applications. This causes a sharp reduction in the incidence of road accidents. Geographically, the ultrasonic sensor market recorded the highest growth in the Asia-Pacific (APAC) region during the last few years and is also predicted to demonstrate the fastest growth in this region in the coming years. The main factors propelling the advancement of the market are the soaring automobile manufacturing and the booming industrial manufacturing sector, primarily in India, China, and Thailand. Additionally, the rising requirement for smart farming equipment will propel the market growth in the region in the future. Hence, it can be said with confidence that the market will register huge growth around the world in the upcoming years, mainly because of the mushrooming usage of ultrasonic sensors in vehicles and various manufacturing operations. Read More: https://www.psmarketresearch.com/market-analysis/ultrasonic-sensor-market0 Comentários 0 Compartilhamentos 7K Visualizações 0 Anterior -

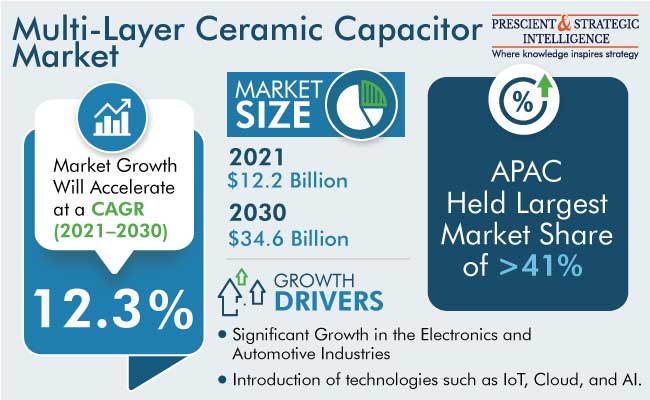

Multi-Layer Ceramic Capacitors WERE Mostly Used in Automotive Industry All Over the World

The multi-layer ceramic capacitor market will advance at a rate of 12.3% in the years to come, to reach USD 34.6 billion by 2030.

The automotive category led the industry, with USD 4.8 billion revenue in the past, which will grow at a rate of about 12.4% in the future.

The major factors powering the requirement for MLCCs in the automotive sector are the snowballing acceptance of EV and autonomous vehicles, regulations of the government for compulsory ADAS systems, and the growing implementation of smart technologies for manufacturing of vehicles.

X7R dielectric type led the industry with a share of about 30.1% in the past, as X7R capacitors have a supreme working temperature and are temperature steady.

Furthermore, this kind of ceramic dielectric capacitors are suitable for frequency discriminating circuits, along with decoupling and bypass applications.

These dielectric MLCCs are also used for filtration and transient voltage suppression. Hence, these factors are responsible for the growth of the industry.

Conversely, the X5R category will grow the fastest in the years to come powering at a rate of 14.2%. This has a lot to do with its increasing acceptance in mobile devices, for instance wearables, portable gadgets, smartphones, and vehicle mounted electronics, and gaming machines, which will surge the requirement for X5R MLCCs.

The high-range voltage category had the largest share, of 48.2%, in the past

This is due to the fact that cutting-edge ceramic dielectric thin-layers and multi-layering approaches are put to use in high-range voltage MLCC capacitors for delivering high capacitance and high voltage to electronic systems.

These are also used in numerous applications, as well as high-voltage coupling capacitors, inverter circuits, lighting ballasts, and switched-mode power supply systems.

APAC led the multi-layer ceramic capacitor market in the past, with USD 5.1 billion, and this trend will continue in the years to come, powering at the highest rate of 13%.

This is because of the growing use of MLCC-based electronic mechanisms and products of renewable energy in the automobile industry. This is also as a result of the growing requirement for MLCCs from end-use industries, on account of their enhanced capacitance levels and capacitor shrinking.

Also, regional MLCC producers are putting efforts toward the adoption upgraded technology for completing efficiently. China is among the big manufacturers of MLCCs, with a substantial presence in the local circuit.

Chinese MLCC producers are expanding quickly in the recent past, emphasized consumer electronics supply.

It is because of the introduction of modern technologies such as IoT, cloud and AI, the demand for multi-layer ceramic capacitor will continue to grow in the years to come, all over the globe.

Read More: https://www.psmarketresearch.com/market-analysis/multi-layer-ceramic-capacitor-mlcc-marketMulti-Layer Ceramic Capacitors WERE Mostly Used in Automotive Industry All Over the World The multi-layer ceramic capacitor market will advance at a rate of 12.3% in the years to come, to reach USD 34.6 billion by 2030. The automotive category led the industry, with USD 4.8 billion revenue in the past, which will grow at a rate of about 12.4% in the future. The major factors powering the requirement for MLCCs in the automotive sector are the snowballing acceptance of EV and autonomous vehicles, regulations of the government for compulsory ADAS systems, and the growing implementation of smart technologies for manufacturing of vehicles. X7R dielectric type led the industry with a share of about 30.1% in the past, as X7R capacitors have a supreme working temperature and are temperature steady. Furthermore, this kind of ceramic dielectric capacitors are suitable for frequency discriminating circuits, along with decoupling and bypass applications. These dielectric MLCCs are also used for filtration and transient voltage suppression. Hence, these factors are responsible for the growth of the industry. Conversely, the X5R category will grow the fastest in the years to come powering at a rate of 14.2%. This has a lot to do with its increasing acceptance in mobile devices, for instance wearables, portable gadgets, smartphones, and vehicle mounted electronics, and gaming machines, which will surge the requirement for X5R MLCCs. The high-range voltage category had the largest share, of 48.2%, in the past This is due to the fact that cutting-edge ceramic dielectric thin-layers and multi-layering approaches are put to use in high-range voltage MLCC capacitors for delivering high capacitance and high voltage to electronic systems. These are also used in numerous applications, as well as high-voltage coupling capacitors, inverter circuits, lighting ballasts, and switched-mode power supply systems. APAC led the multi-layer ceramic capacitor market in the past, with USD 5.1 billion, and this trend will continue in the years to come, powering at the highest rate of 13%. This is because of the growing use of MLCC-based electronic mechanisms and products of renewable energy in the automobile industry. This is also as a result of the growing requirement for MLCCs from end-use industries, on account of their enhanced capacitance levels and capacitor shrinking. Also, regional MLCC producers are putting efforts toward the adoption upgraded technology for completing efficiently. China is among the big manufacturers of MLCCs, with a substantial presence in the local circuit. Chinese MLCC producers are expanding quickly in the recent past, emphasized consumer electronics supply. It is because of the introduction of modern technologies such as IoT, cloud and AI, the demand for multi-layer ceramic capacitor will continue to grow in the years to come, all over the globe. Read More: https://www.psmarketresearch.com/market-analysis/multi-layer-ceramic-capacitor-mlcc-market0 Comentários 0 Compartilhamentos 6K Visualizações 0 Anterior -

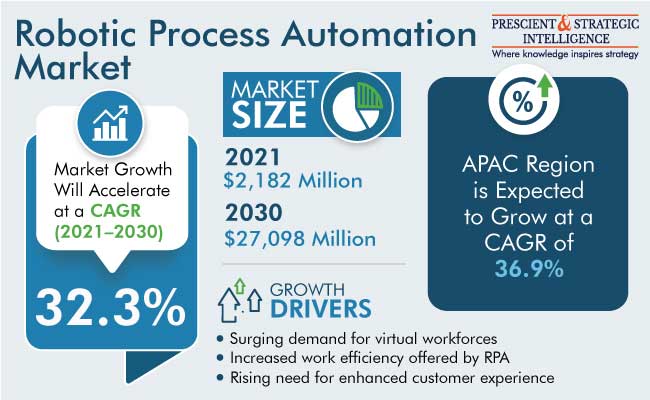

What Does RPA Decrease Human Requirement in Repetitive Work Processes?

The robotic process automation industry has garnered $2,182 million revenue, and it is projected to experience a growth at a rate of 32.3% from 2021 to 2030. The major factors for industry growth include easy handling of business processes, better customer experience, and higher efficiency provided by RPA solutions.

Robotic process automation is an advanced software technology that contributes to building, deploying, and managing software robots that imitate the actions of humans and interact with digital software and systems.

Software category is projected to experience faster growth, rising at a rate of 34.9% in the coming future. It is ascribed to the surging adoption of RPA software across various verticals to boost efficiency and mitigate time wastage.

Software robots can also perform things to understand what is on the screen, navigation systems, right keystrokes, identification and extraction of data, along with various other actions more quickly compared to humans.

Enterprises get advanced with high efficiency, productivity, and resilience. From the financial to healthcare and manufacturing sectors, companies have implemented RPA in various areas such as compliance, legal, finance, operations, customer service, and information technology.

RPA is ideal for virtually any business-rules-driven, high-volume, repeatable process for automation. It also boosts the efficiency of cognitive processes that need advanced AI skills.

RPA provides support to various types of industries to resolve specific operation issues in advanced and powerful ways.

Leaders in various sectors from finance to marketing, customer service to human resources, and beyond need RPA to improve various processes, achieve higher capacity, fewer errors, and faster throughput for major processes.

From senior management or CFO’s perspective, RPA technology investment offers quick ROI and needs minimal upfront expenditure compared to other technologies in enterprises.

The implementation of RPA causes no little or negligible disruption. That is why software robots can easily access and function within legacy systems. RPA is a major digital transformation enabler.

The retail and consumer goods category are projected to experience the fastest growth in the industry in the coming future. It is ascribed to numerous advantages provided to companies operating in the retail and consumer sector. It includes cost savings from unnecessary expenditure on resources and better revenue management.

The automated solution category holds the largest industry share, of 48%, and it is projected to follow the same trend in the coming future. It is ascribed to rising efforts to automate basic processes such as data entry, customer query handling, information verification, and uploading for automatic rejections and approvals.

The major companies operating in the industry are; Pegasystems Inc., Celaton Ltd., Xerox Corporation, IBM Corporation, Blue Prism Limited, NICE Ltd., IPsoft Incorporated, and UiPath.

Therefore, the high efficiency offered by software robots boosts the demand for robotic process automation.

Read More: https://www.psmarketresearch.com/market-analysis/robotic-process-automation-marketWhat Does RPA Decrease Human Requirement in Repetitive Work Processes? The robotic process automation industry has garnered $2,182 million revenue, and it is projected to experience a growth at a rate of 32.3% from 2021 to 2030. The major factors for industry growth include easy handling of business processes, better customer experience, and higher efficiency provided by RPA solutions. Robotic process automation is an advanced software technology that contributes to building, deploying, and managing software robots that imitate the actions of humans and interact with digital software and systems. Software category is projected to experience faster growth, rising at a rate of 34.9% in the coming future. It is ascribed to the surging adoption of RPA software across various verticals to boost efficiency and mitigate time wastage. Software robots can also perform things to understand what is on the screen, navigation systems, right keystrokes, identification and extraction of data, along with various other actions more quickly compared to humans. Enterprises get advanced with high efficiency, productivity, and resilience. From the financial to healthcare and manufacturing sectors, companies have implemented RPA in various areas such as compliance, legal, finance, operations, customer service, and information technology. RPA is ideal for virtually any business-rules-driven, high-volume, repeatable process for automation. It also boosts the efficiency of cognitive processes that need advanced AI skills. RPA provides support to various types of industries to resolve specific operation issues in advanced and powerful ways. Leaders in various sectors from finance to marketing, customer service to human resources, and beyond need RPA to improve various processes, achieve higher capacity, fewer errors, and faster throughput for major processes. From senior management or CFO’s perspective, RPA technology investment offers quick ROI and needs minimal upfront expenditure compared to other technologies in enterprises. The implementation of RPA causes no little or negligible disruption. That is why software robots can easily access and function within legacy systems. RPA is a major digital transformation enabler. The retail and consumer goods category are projected to experience the fastest growth in the industry in the coming future. It is ascribed to numerous advantages provided to companies operating in the retail and consumer sector. It includes cost savings from unnecessary expenditure on resources and better revenue management. The automated solution category holds the largest industry share, of 48%, and it is projected to follow the same trend in the coming future. It is ascribed to rising efforts to automate basic processes such as data entry, customer query handling, information verification, and uploading for automatic rejections and approvals. The major companies operating in the industry are; Pegasystems Inc., Celaton Ltd., Xerox Corporation, IBM Corporation, Blue Prism Limited, NICE Ltd., IPsoft Incorporated, and UiPath. Therefore, the high efficiency offered by software robots boosts the demand for robotic process automation. Read More: https://www.psmarketresearch.com/market-analysis/robotic-process-automation-market0 Comentários 0 Compartilhamentos 6K Visualizações 0 Anterior -

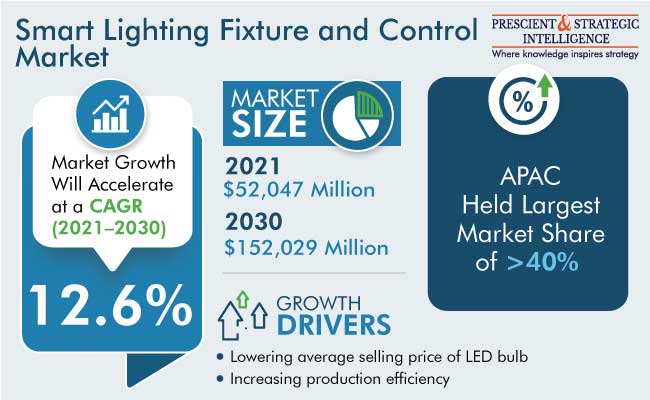

APAC Is the Dominating Smart Light Fixture and Control Market

The smart light fixture and control market was valued at $52,047 million in 2021, and it is set to reach $152,029 million by 2030, growing at a CAGR of 12.6% between 2021 and 2030, according to a research report by a market research company P&S Intelligence. This growth can be ascribed to the dropping of average retailing price of LED bulbs credited to the growing production efficiency and reduced material prices.

Furthermore, the emerging problem of the energy crisis is forcing governments and people to shift toward smart lights, which can reduce the consumption of electricity.

The smart lighting industry is already popular in developed countries and is projected to grow significantly in developing countries also in the years to come. As the government has taken several initiatives to encourage the use of smart lights to reduce energy consumption.

LED lights will dominate the smart light fixture market in the future. This can be credited to the several benefits of this technology, including its low costs and better illumination effectiveness than traditional lights.

The smart light control is a network of numerous lighting fixtures linked together to control smart systems. The industry is growing mainly because of the increased pace of technological enhancement and continuous development in smart controls.

With the usage of dependable procedures and distributed control systems, controllers provide significant lighting functionality and customer value, performance, and energy effectiveness.

In 2021, the offline channel category held the larger share, mainly because instructions for installations for light fixtures are offered in detail by the salesman, helps in choosing high-quality items.

APAC held the largest share of approximately 40% in the past. This can be ascribed to the increasing initiatives by the governments of developing economies to encourage the usage of energy-efficient lights.

In addition, to draw customers' attention, key players are spending heavily on advertising their products in hospitals, schools, malls, salons, and other public places, also the rising acceptance of smart cities is contributing to the growth of the demand for energy-saving products like LED lights.

Moreover, the per-capita income of people is on the rise, which encourages them to switch to high-tech systems, propelling the demand in the region.

North America held a significant revenue share in the past, in which the U.S. dominated the region, due to the growing requirement for wireless lighting fixtures. The major benefits of these products include programming flexibility, energy efficiency, extended lifespan, and long-distance control are motivating the leading companies in the region to produce wireless lighting fixtures.

The dropping average retailing price of LED bulbs and several government initiatives to encourage the use of these lights will drive the demand for smart light fixture and control systems.

Read More: https://www.psmarketresearch.com/market-analysis/smart-light-fixture-and-control-marketAPAC Is the Dominating Smart Light Fixture and Control Market The smart light fixture and control market was valued at $52,047 million in 2021, and it is set to reach $152,029 million by 2030, growing at a CAGR of 12.6% between 2021 and 2030, according to a research report by a market research company P&S Intelligence. This growth can be ascribed to the dropping of average retailing price of LED bulbs credited to the growing production efficiency and reduced material prices. Furthermore, the emerging problem of the energy crisis is forcing governments and people to shift toward smart lights, which can reduce the consumption of electricity. The smart lighting industry is already popular in developed countries and is projected to grow significantly in developing countries also in the years to come. As the government has taken several initiatives to encourage the use of smart lights to reduce energy consumption. LED lights will dominate the smart light fixture market in the future. This can be credited to the several benefits of this technology, including its low costs and better illumination effectiveness than traditional lights. The smart light control is a network of numerous lighting fixtures linked together to control smart systems. The industry is growing mainly because of the increased pace of technological enhancement and continuous development in smart controls. With the usage of dependable procedures and distributed control systems, controllers provide significant lighting functionality and customer value, performance, and energy effectiveness. In 2021, the offline channel category held the larger share, mainly because instructions for installations for light fixtures are offered in detail by the salesman, helps in choosing high-quality items. APAC held the largest share of approximately 40% in the past. This can be ascribed to the increasing initiatives by the governments of developing economies to encourage the usage of energy-efficient lights. In addition, to draw customers' attention, key players are spending heavily on advertising their products in hospitals, schools, malls, salons, and other public places, also the rising acceptance of smart cities is contributing to the growth of the demand for energy-saving products like LED lights. Moreover, the per-capita income of people is on the rise, which encourages them to switch to high-tech systems, propelling the demand in the region. North America held a significant revenue share in the past, in which the U.S. dominated the region, due to the growing requirement for wireless lighting fixtures. The major benefits of these products include programming flexibility, energy efficiency, extended lifespan, and long-distance control are motivating the leading companies in the region to produce wireless lighting fixtures. The dropping average retailing price of LED bulbs and several government initiatives to encourage the use of these lights will drive the demand for smart light fixture and control systems. Read More: https://www.psmarketresearch.com/market-analysis/smart-light-fixture-and-control-market0 Comentários 0 Compartilhamentos 3K Visualizações 0 Anterior -

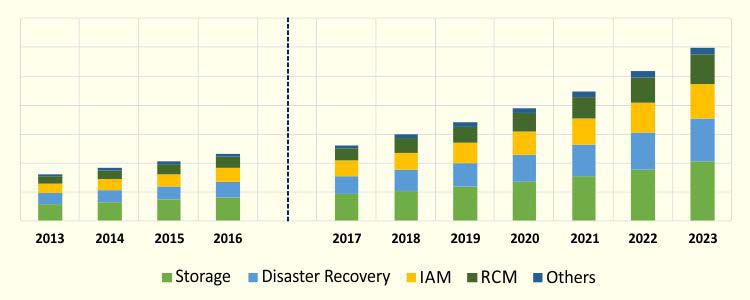

How Are Technological Advancements Fueling Government Cloud Market Growth?

Growth factors like the rapid digitalization of government organizations and need to reduce the total cost of ownership (TCO) will drive the government cloud market at a CAGR of 15.4% during the forecast period (2017–2023), since generating revenue of $20.8 billion in 2017. Moreover, the constant improvements in cloud computing technologies and rapid advancements in public-sector technology solutions will facilitate the market growth. Additionally, the innovations in the internet of things (IoT) technology will encourage governments to adopt cloud solutions.

Government bodies are increasingly deploying cloud-based solutions to reduce their capital expenditure (CAPEX) without compromising the important public services. The utilization of the cloud is allowing such agencies to decrease the TCO of services, directly and indirectly. Moreover, the increasing need for facility consolidation, labor optimization, asset utilization, and measured services has propelled the adoption of the cloud technology in government organizations. Additionally, government stakeholders are switching to the cloud platform due to the integration of advanced technologies in their daily operations.

Currently, technological innovations have become a key trend in the government cloud market. Moreover, the rising number of e-government initiatives are amplifying the adoption of cloud computing. This is allowing governments to enhance their business flexibility in spite of their back-end silo systems. Departments such as education, defense, and insurance are some of the early users of cloud computing in the public sector. Further, technological developments and the high penetration of the internet will raise the demand for cloud computing in other government departments and ministries as well.

Besides, a surge in the IoT usage is fueling the adoption of cloud solutions, thereby creating lucrative opportunities for the players in the government cloud market. The Deployment of IoT needs cloud-based technologies to improve the connectivity between several devices, which is provided through private, public, and hybrid models. Additionally, technological transformation on account of the hefty investments in the IoT and cloud solutions will boost the application of the cloud in the public sector. Furthermore, the government sector is comprehending the importance of IoT for obtaining in-depth analysis and deriving vital information for the same.

The categories under the model segment of the government cloud market include platform as a service (PaaS), software as a service (SaaS), and infrastructure as a service (IaaS). Among these, the SaaS category generated the highest revenue in 2017. This can be ascribed to the wide-scale deployment of the SaaS model in government organizations due to the low-cost and pay-as-you-go capability offered by them. Moreover, government organizations are adopting the SaaS model to rent software applications from cloud service providers (CSP).

North America held the largest share in the government cloud market in 2017, and it will continue its dominance in the forecast years due to the huge investments by government organizations in cloud-based solutions. The Asia-Pacific (APAC) market will witness the fastest growth during the forecast period owing to the growing investments in the information and communication technology (ICT) sector, amplifying promotional campaigns, and rising focus of governments on improving citizen services. Besides, the increasing requirement for cloud-based security services, to enhance accessibility and strengthen decision making, will drive the market.

Thus, the rising integration of the IoT and cloud computing in government agencies will fuel the market growth in the future.

Read More: https://www.psmarketresearch.com/market-analysis/government-cloud-marketHow Are Technological Advancements Fueling Government Cloud Market Growth? Growth factors like the rapid digitalization of government organizations and need to reduce the total cost of ownership (TCO) will drive the government cloud market at a CAGR of 15.4% during the forecast period (2017–2023), since generating revenue of $20.8 billion in 2017. Moreover, the constant improvements in cloud computing technologies and rapid advancements in public-sector technology solutions will facilitate the market growth. Additionally, the innovations in the internet of things (IoT) technology will encourage governments to adopt cloud solutions. Government bodies are increasingly deploying cloud-based solutions to reduce their capital expenditure (CAPEX) without compromising the important public services. The utilization of the cloud is allowing such agencies to decrease the TCO of services, directly and indirectly. Moreover, the increasing need for facility consolidation, labor optimization, asset utilization, and measured services has propelled the adoption of the cloud technology in government organizations. Additionally, government stakeholders are switching to the cloud platform due to the integration of advanced technologies in their daily operations. Currently, technological innovations have become a key trend in the government cloud market. Moreover, the rising number of e-government initiatives are amplifying the adoption of cloud computing. This is allowing governments to enhance their business flexibility in spite of their back-end silo systems. Departments such as education, defense, and insurance are some of the early users of cloud computing in the public sector. Further, technological developments and the high penetration of the internet will raise the demand for cloud computing in other government departments and ministries as well. Besides, a surge in the IoT usage is fueling the adoption of cloud solutions, thereby creating lucrative opportunities for the players in the government cloud market. The Deployment of IoT needs cloud-based technologies to improve the connectivity between several devices, which is provided through private, public, and hybrid models. Additionally, technological transformation on account of the hefty investments in the IoT and cloud solutions will boost the application of the cloud in the public sector. Furthermore, the government sector is comprehending the importance of IoT for obtaining in-depth analysis and deriving vital information for the same. The categories under the model segment of the government cloud market include platform as a service (PaaS), software as a service (SaaS), and infrastructure as a service (IaaS). Among these, the SaaS category generated the highest revenue in 2017. This can be ascribed to the wide-scale deployment of the SaaS model in government organizations due to the low-cost and pay-as-you-go capability offered by them. Moreover, government organizations are adopting the SaaS model to rent software applications from cloud service providers (CSP). North America held the largest share in the government cloud market in 2017, and it will continue its dominance in the forecast years due to the huge investments by government organizations in cloud-based solutions. The Asia-Pacific (APAC) market will witness the fastest growth during the forecast period owing to the growing investments in the information and communication technology (ICT) sector, amplifying promotional campaigns, and rising focus of governments on improving citizen services. Besides, the increasing requirement for cloud-based security services, to enhance accessibility and strengthen decision making, will drive the market. Thus, the rising integration of the IoT and cloud computing in government agencies will fuel the market growth in the future. Read More: https://www.psmarketresearch.com/market-analysis/government-cloud-market0 Comentários 0 Compartilhamentos 6K Visualizações 0 Anterior

Mais Stories