Adhesive Films—Scale, Segmentation, and Asia-Pacific Momentum

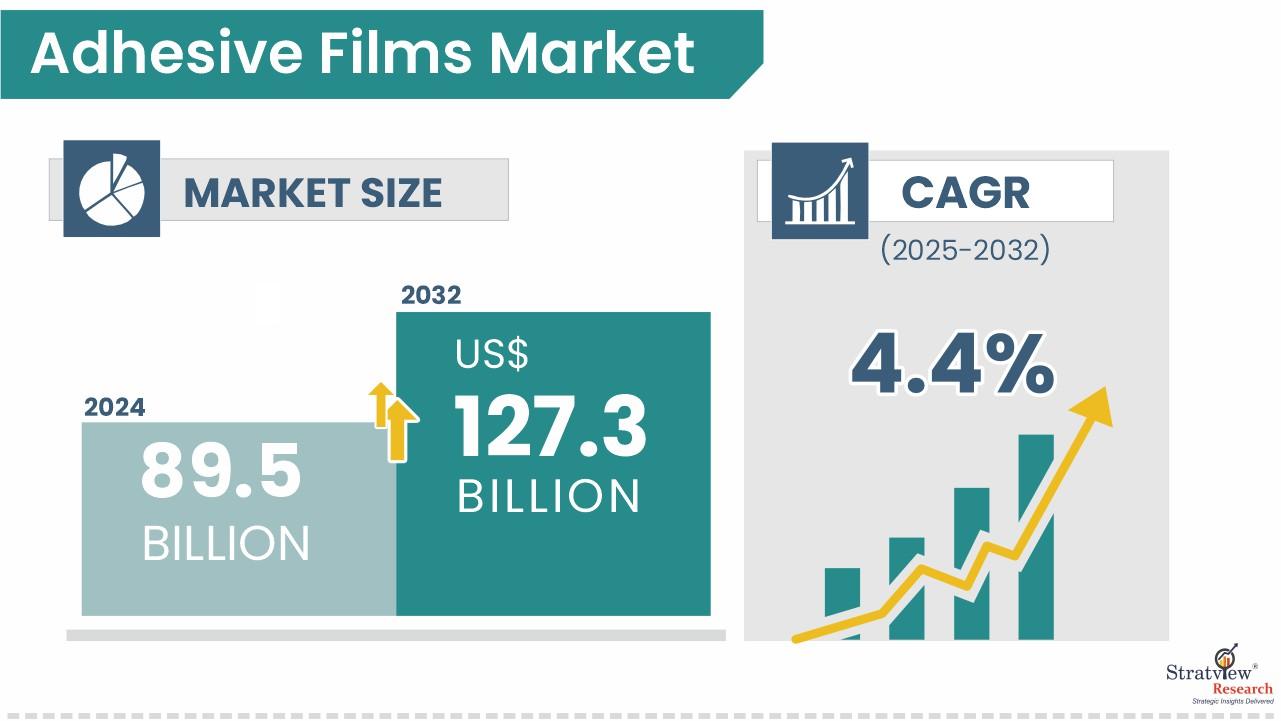

Adhesive films—thin layers of polymer coated with pressure-sensitive, heat-activated, or other adhesive chemistries—have become foundational in packaging, labels, graphics, electronics assembly, and a widening range of industrial uses. According to Stratview Research, the global adhesive films market was estimated at USD 89.5 billion in 2024 and is projected to reach USD 127.3 billion by 2032, reflecting a 4.4% CAGR during 2025–2032.

Request the sample report here:

https://stratviewresearch.com/Request-Sample/3710/adhesive-films-market.html#form

Drivers

The most visible catalyst is packaging and labeling modernization. As consumer brands compress design cycles and expand SKUs, high-quality label stock, over-laminates, and tamper-evident features all translate into higher value per square meter of film. Meanwhile, the boom in e-commerce and fast-moving consumer goods keeps volumes elevated across label and protective formats—segments where adhesive films are the default bonding and functional layer.

Electronics is the second key engine. From smartphones and wearables to white goods and EV battery modules, device designers prefer clean, uniform, low-profile bonding—precisely what films deliver. Films also contribute optical clarity, die-cut precision, vibration damping, and thermal management when paired with specialty chemistries and backings. In high-throughput assembly, die-cut films outperform liquid adhesives by reducing mess, cure time, and rework.

Automotive and transportation add a durable base of structural and semi-structural tasks: emblem mounting, wire harness wrapping, vibration damping, trim attachment, and paint protection stacks. As interiors digitize and exterior surfaces become more functional (lighting, sensing), film-based solutions gain share over mechanical fasteners, particularly where weight, aesthetics, or mixed-material bonding are constraints.

Stratview’s segmentation underscores where demand concentrates. By resin chemistry, acrylic systems are anticipated to remain the largest demand generator, given their balanced adhesion, aging resistance, and optical performance. On the materials side, polypropylene (PP), polyvinyl chloride (PVC), and polyethylene (PE) remain the primary backing films, spanning commodity applications through to premium, specialty constructions. Regionally, Asia-Pacific is expected to remain the largest market through the forecast window, reflecting the region’s manufacturing depth in packaging, electronics, and automotive supply chains.

Challenges

Three execution hurdles stand out. First, sustainability pressure is real: brand owners and regulators want lower VOCs, higher recycled content, and mono-material packaging that enables recycling without delamination headaches. Converting multi-layer structures toward recyclable or biodegradable configurations, while preserving performance and line speed, demands reformulation and often new capital equipment.

Second, cost and availability of feedstocks can be volatile. Fluctuations in monomers, solvents, and film resins (PP, PVC, PE) ripple into adhesive coat-weights and total applied cost. Suppliers must balance performance targets with cost-in-use, optimize coat-weight, and standardize SKUs to protect margins through cycles.

Third, technical demands are rising. Electronics and medical uses require very low outgassing, stable adhesion on low-surface-energy substrates, optical purity, and clean die-cutting—tightening tolerances on gel count, haze, and particulate control. For transportation and outdoor graphics, UV/weatherability and long-term peel/shear retention remain gating factors. The burden shifts upstream to resin selection, tackifier systems, crosslinking methods, and clean-room converting discipline.

Conclusion

With a market rising from USD 89.5 billion (2024) to USD 127.3 billion by 2032 at 4.4% CAGR, adhesive films are positioned for steady, secular growth. Expect acrylic chemistries and PP/PVC/PE backings to keep anchoring the product mix, while Asia-Pacific continues to set the volume and cost curve for global supply. The winners will pair chemistry know-how with converting excellence and sustainability roadmaps—simplifying recycling, lowering VOCs/solvents, and enabling mono-material packaging where possible. Those who can deliver high-clarity optics for electronics, durable outdoor performance for graphics, and robust, clean assembly for automotive will capture premium share as specifications tighten and the value per square meter rises.