Automotive Lead Acid Battery Market Analysis Reveals Trends, Growth Drivers, and Regional Performance Insights

The automotive lead acid battery market remains a cornerstone of the global automotive energy storage landscape. Despite rising competition from advanced battery technologies, lead acid batteries continue to hold a dominant position in both developed and emerging markets. This analysis explores key market dynamics, regional performance, technology developments, and future outlooks shaping the trajectory of this longstanding energy solution.

Current Market Structure and Demand Patterns

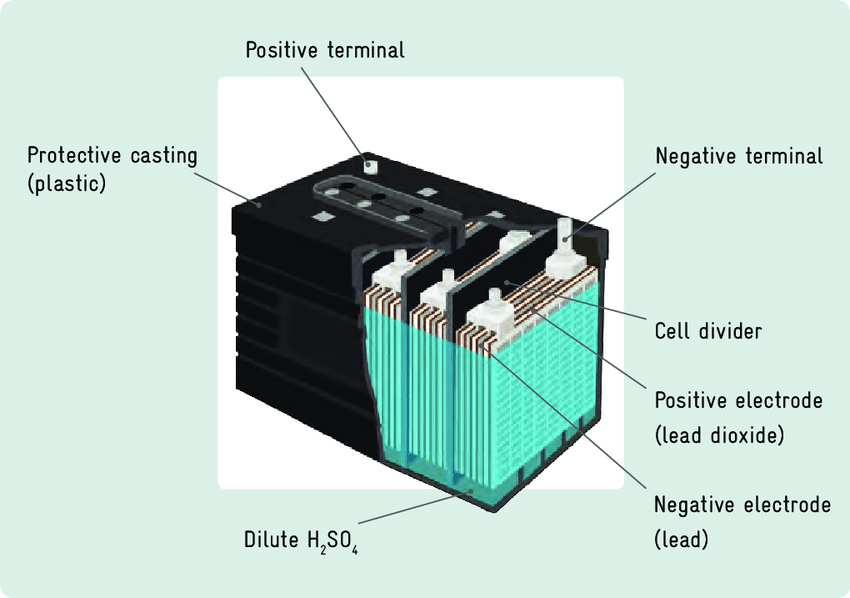

The market for automotive lead acid batteries is segmented primarily into two categories: starting, lighting, and ignition (SLI) batteries and advanced lead acid batteries such as enhanced flooded batteries (EFB) and absorbent glass mat (AGM) batteries. SLI batteries represent the majority of demand, serving internal combustion engine (ICE) vehicles globally. However, with the growth of vehicles equipped with start-stop systems, the demand for more durable and efficient EFB and AGM batteries is rapidly increasing.

Passenger cars remain the dominant application segment, but the commercial vehicle sector is also contributing significantly to demand. With the expanding logistics and transport sector in emerging markets, the need for reliable and affordable battery technologies has pushed lead acid batteries to the forefront due to their established performance and low cost.

Key Trends Driving Market Dynamics

Several major trends are currently shaping the automotive lead acid battery market:

-

Steady Vehicle Electrification

While lithium-ion batteries power the propulsion systems in electric vehicles (EVs), lead acid batteries continue to be used for secondary or auxiliary functions. Hybrid and electric vehicles still require these batteries for operations such as electronics, HVAC, and security systems. As EV adoption grows, so does the demand for high-quality auxiliary lead acid batteries. -

Rising Aftermarket Demand

Due to the relatively shorter lifecycle of lead acid batteries—typically 3 to 5 years—there is consistent demand in the aftermarket segment. Consumers routinely replace their batteries, especially in regions with extreme climates that shorten battery life. The availability, affordability, and widespread servicing options for lead acid batteries ensure their continued prominence in the aftermarket. -

Shift Toward Maintenance-Free Technologies

Consumers are showing preference for maintenance-free battery solutions. This trend has led to increased adoption of AGM and EFB batteries, which offer sealed, spill-proof designs and enhanced durability. This evolution supports vehicles equipped with advanced electronic systems and start-stop capabilities. -

Environmental Sustainability and Circular Economy

Lead acid batteries boast one of the highest recycling rates among energy storage technologies. Over 95% of a typical lead acid battery can be recycled and reused, including the lead, plastic casing, and sulfuric acid. This efficiency aligns with global sustainability goals and strengthens the position of lead acid batteries in eco-conscious markets.

Regional Performance and Market Leaders

Geographically, Asia-Pacific holds the largest share of the automotive lead acid battery market. This is due to the sheer volume of vehicle production and sales in countries such as China, India, and Japan. The region also benefits from strong manufacturing infrastructure and rising demand for both new vehicles and aftermarket services.

North America and Europe follow, with mature markets that are seeing a transition toward advanced lead acid technologies. In these regions, high vehicle ownership rates, established recycling programs, and increasing hybrid vehicle penetration drive stable demand. Meanwhile, in Latin America, the Middle East, and Africa, affordability remains a key purchasing factor, favoring traditional lead acid battery formats.

Key players in the market continue to invest in research and development to improve battery life, charge retention, and power output. The competition remains intense, with manufacturers striving to offer both value and innovation to retain their market share.

Challenges and Competitive Landscape

Despite its strengths, the lead acid battery market faces certain challenges:

-

Technological Competition: Lithium-ion and other next-generation battery technologies are gaining traction, especially in full EV segments, posing a long-term threat to lead acid battery usage.

-

Weight and Energy Density: Compared to newer technologies, lead acid batteries have lower energy-to-weight ratios, which limits their application in advanced mobility solutions.

-

Regulatory Pressure: Environmental regulations on lead usage, especially in developed countries, could tighten further, requiring improved manufacturing and recycling practices.

Yet, due to cost advantages, reliability, and recyclability, the market is expected to remain stable and evolve with technological enhancements.

Future Outlook

The automotive lead acid battery market is projected to maintain steady growth in the coming years, supported by ongoing demand from ICE vehicles, growth in hybrid models, and the resilience of aftermarket sales. Technological innovation in battery design and sustainability practices will be key to ensuring the continued relevance of lead acid batteries in a rapidly transforming global automotive ecosystem.

While the spotlight may increasingly turn toward advanced chemistries, the value proposition of lead acid batteries—durability, cost-efficiency, and circular economy compatibility—continues to make them an indispensable component of today’s automotive energy mix.