Bone Cancer Treatment Market Price, Trends, Growth, Analysis, Key Players, Outlook, Report, Forecast 2025-2032

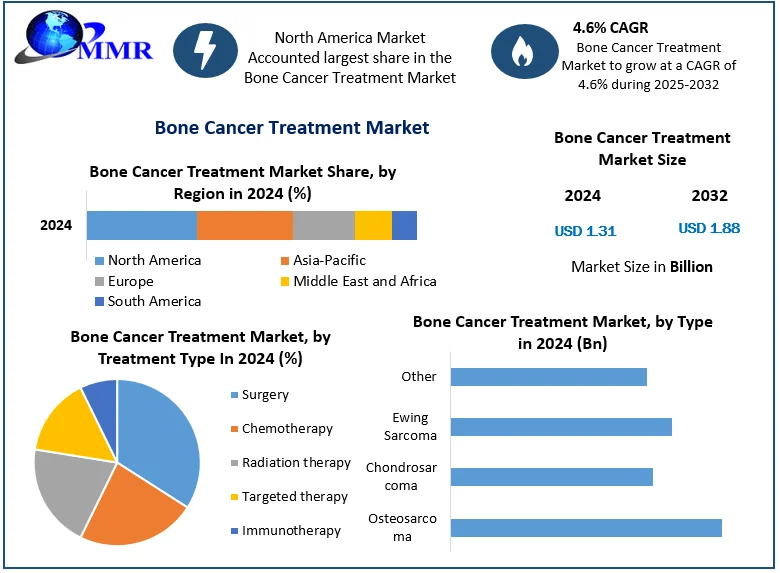

bone cancer treatment market, valued at an estimated USD 1.90 billion in 2023, is projected to grow to USD 3.15 billion by 2030, achieving a CAGR of approximately 7.3%. Growth is propelled by increasing incidence of primary and metastatic bone cancers, advancements in targeted therapies, and a surge in R&D collaboration across pharmaceutical and biotech sectors.

Request Free Sample Report:https://www.maximizemarketresearch.com/request-sample/221663/

1. Market Estimation, Growth Drivers & Opportunities

Bone cancers include both primary tumors (e.g., osteosarcoma, Ewing’s sarcoma, chondrosarcoma) and secondary bone metastases, commonly originating from breast, prostate, or lung cancers.

Key growth drivers:

-

A rising global incidence of bone metastases, driven by extended survivorship in breast and prostate cancers.

-

Enhanced early diagnosis through advanced imaging and biomarker use.

-

Development of novel targeted agents—such as next-gen bisphosphonates, denosumab, mTOR inhibitors, and immunotherapies.

-

A shift toward personalized and combination treatments, emphasizing precision medicine.

Opportunities include:

-

Research into CAR-T therapies that specifically target bone tumor antigens.

-

Approval of oral bone-targeted radiopharmaceuticals allowing outpatient treatment.

-

Growth in emerging markets with expanding oncology infrastructure and increasing diagnosis rates.

2. U.S. Market Trends & Investments (2024–2025)

The U.S. market leads globally, accounting for approximately 43% of 2024 sales. Highlights include:

-

The FDA approval of Pluvicto® (a bone-targeting radioligand for prostate cancer metastases) in late 2024, boosting uptake.

-

Additional clinical advancements in Lutetium-177-PSMA therapies and bone-directed immunotherapies.

-

Several Phase II/III trials in metastatic osteosarcoma utilizing novel agents like MCLA-158 (bispecific ADC).

-

Multi-million-dollar funding from the National Cancer Institute to develop bone-targeted nano-carriers to reduce therapy toxicity.

These trends underscore the U.S. as a robust innovation hub with strong regulatory and clinical foundations driving market expansion.

3. Market Segmentation – Segments with Largest Share

Key market segments by share include:

-

Therapy Type: Bisphosphonates and RANKL inhibitors (e.g., denosumab) dominate due to frequent off-label use in metastases and supportive care regimens.

-

Administration Route: Intravenous therapies account for the largest market share, favored for hospital- or infusion center-based treatments. Oral bisphosphonates follow closely.

-

Cancer Type: Bone metastases (primarily from breast and prostate) represent the largest value segment, driven by high incidence and ongoing adjuvant treatment use.

-

End-User: Hospitals and oncology clinics dominate treatment delivery, followed by specialized cancer centers and home infusion services.

4. Competitive Analysis – Top 5 Global Players

Leading companies shaping the market are:

-

Amgen Inc.

As the developer of denosumab, Amgen leads bone-targeted therapy and is exploring new indications and delivery formats to enhance patient convenience. -

Novartis AG

Manufactures zoledronic acid (Zometa®) and is advancing pipelines involving bone-targeted kinase inhibitors and therapies used in aggressive bone sarcomas. -

Bayer AG

Through its radiopharmaceutical portfolio, Bayer is advancing Radium-223 analogs and emerging bone-targeted therapies in metastatic castration-resistant prostate cancer. -

Pfizer Inc.

Pfizer continues to support bisphosphonate use and is investing in next-gen bone-targeted agents, including injectable hormonal modulators and ADC prototypes. -

Bristol‑Myers Squibb (BMS)

With a growing presence in immuno-oncology, BMS is testing B7-H3 and GD2-targeted ADCs for bone metastases and sarcoma in late-stage trials.

These companies are forging collaborations with research institutions, advancing clinical trials, and optimizing drug delivery to improve efficacy and reduce side effects.

5. Regional Analysis – USA, UK, Germany, France, Japan, China

-

United States: The top market globally, driven by reimbursement coverage, advanced clinical trial infrastructure, and access to cutting-edge therapies.

-

United Kingdom: The NHS supports emerging therapies through its Cancer Drug Fund, improving access to novel bone-targeted treatments and promoting early detection initiatives.

-

Germany: Strong public-private partnerships between hospitals and research institutes drive adoption of innovative treatments in sarcoma and metastasis care.

-

France: As part of the EU’s oncology strategy, France invests heavily in early screening programs that support growth in bone-targeted treatments.

-

Japan: A large and aging population leads to a rising rate of bone metastases; Japan has recently approved denosumab for osseous sarcomas.

-

China: One of the fastest-growing regions, fueled by rising cancer prevalence, expanded oncology infrastructure, and government reimbursement policies for novel therapies.

6. Conclusion & Market Outlook

At USD 1.90 billion in 2023, expanding to USD 3.15 billion by 2030 at a CAGR of ~7.3%, the bone cancer treatment market is set for sustained growth.

Related Report:

Biometric payment market:https://www.maximizemarketresearch.com/market-report/biometric-payment-market/190525/

Next generation computing market:https://www.maximizemarketresearch.com/market-report/next-generation-computing-market/190444/