Europe Online Grocery Market To Set Massive CAGR of 23.4% During 2025-2033 | Industry Growth Report by IMARC Group

Market Overview 2025-2033

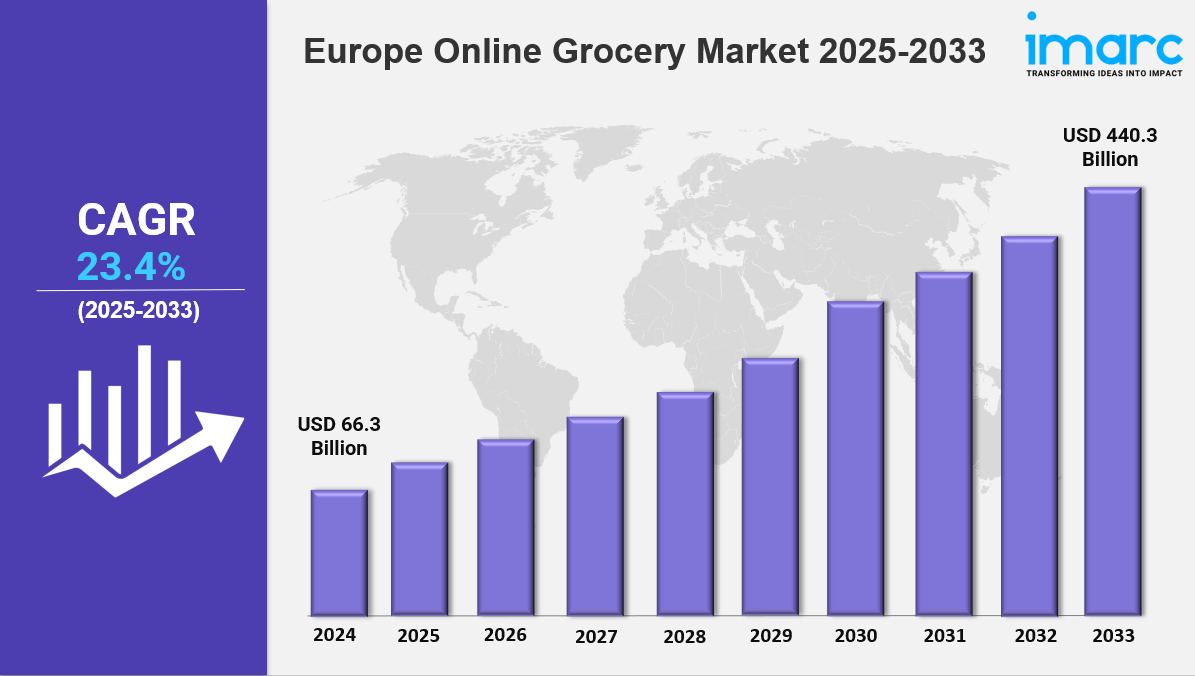

The Europe online grocery market size was valued at USD 66.3 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 440.3 Billion by 2033, exhibiting a CAGR of 23.4% from 2025-2033. The market is expanding rapidly due to growing e-commerce adoption, changing consumer preferences, and convenience-driven shopping habits. Technological advancements, quick delivery services, and digital payment solutions are key factors driving industry growth.

Key Market Highlights:

✔️ Strong market growth driven by increasing digital adoption and demand for convenience

✔️ Rising preference for fresh, organic, and subscription-based grocery deliveries

✔️ Expanding investments in AI-driven logistics, dark stores, and quick commerce solutions

Request for a sample copy of the report: https://www.imarcgroup.com/europe-online-grocery-market/requestsample

Europe Online Grocery Market Trends and Drivers:

The European online grocery market is changing fast. Hyperlocal delivery networks and dark stores are leading this logistics revolution. Dark stores are small fulfillment centers in city areas. By mid-2024, companies like Getir, Gorillas, and Ocado set up over 2,000 dark stores in major cities like London, Berlin, and Paris. This move cuts delivery times to under 15 minutes for 80% of orders. This shift meets consumer demand for quick service. Hybrid work models and smaller households now favor convenience over buying in bulk. However, dark stores require a lot of capital. This need for investment is driving consolidation.

Big players like Amazon Fresh are buying struggling startups, such as Jiffy in the UK, to strengthen their presence in busy areas. Sustainability is also changing these networks. Now, 60% of dark stores use electric cargo bikes. AI tools have helped cut delivery emissions by 25% since 2024. Regulatory pressures, like France’s 2024 ban on single-use plastic delivery packaging, push operators to use reusable containers and carbon-neutral last-mile solutions.

Artificial intelligence is redefining customer engagement in Europe’s online grocery sector. Advanced algorithms now analyze purchasing patterns, dietary preferences, and even real-time fridge inventory (via IoT-enabled smart appliances) to generate hyper-personalized shopping lists. By late 2024, platforms like Picnic (Netherlands) and Rohlik (Czech Republic) reported a 40% increase in average order value after integrating ChatGPT-4o assistants that suggest meal kits based on users’ health goals and cultural preferences. Subscription models have surged, with 35% of European households enrolled in curated grocery boxes—ranging from Carrefour’s “Zero-Waste Chef” bundles to HelloFresh’s AI-adjusted recipes accommodating regional taste trends.

This dynamic is monetizing data at unprecedented scales: Retailers now license anonymized shopping insights to CPG brands, creating a $3.2 billion B2B analytics submarket. However, privacy concerns linger, prompting the EU’s 2024 Digital Grocery Act to mandate opt-in consent for data usage, slowing algorithmic refinement in price-sensitive markets like Southern Europe. Consumer demand for eco-accountability is radically altering supply chains. Over 70% of online grocers in Europe now require suppliers to have Science-Based Targets initiative (SBTi) certifications. This move phases out vendors using air-freighted produce or non-recyclable packaging. In 2024, Germany’s Flink launched “Climate Cart” labels.

These labels calculate a product’s carbon footprint using blockchain-tracked logistics data. Partnerships in vertical farming are growing. Ocado’s deal with Infarm allows on-demand delivery of leafy greens grown in warehouses. This method uses 95% less water than traditional agriculture. Also, surplus food platforms like Too Good To Go are now part of mainstream apps. They help divert 1.2 million tons of waste each year. However, these initiatives face challenges in scaling up. Urban vertical farms currently meet only 8% of the demand for organic produce. Still, regulatory support, like the EU’s 2024 Agro-Ecology Subsidy, is boosting investments.

The Europe online grocery market will reach €186 billion by 2025. It is changing due to three main forces: logistics innovation, AI hyper-personalization, and sustainability mandates. A key moment happened in 2024 when the EU’s Digital Services Act applied to e-grocery. This law introduced strict rules on pricing and delivery timelines. At the same time, consumers started to prefer “grocer-tainment.” Platforms like Italy’s Everli now provide live cooking classes and auto-populated ingredient carts, mixing shopping with community engagement.

Geographic differences are clear. Northern Europe excels in tech use. For example, 85% of Swedish households order groceries online each month. In contrast, Southern Europe is behind with only 35%. This is due to a strong cultural tie to physical markets. However, the 2024 heatwave changed things. Spain’s online grocery sales doubled to 28% as people chose to shop indoors. This suggests that climate may shift shopping habits.

Looking ahead, the market’s growth will hinge on bridging the “green premium” gap. Sixty-eight percent of consumers say they will pay more for sustainable options. However, actual purchases of premium products are below 22% outside Scandinavia. New solutions are emerging, like dynamic discounts for low-carbon baskets and blockchain for farm-to-fork traceability. These aim to connect ethical choices with buying actions. As hybrid retail models grow, such as Aldi's click-and-collect hubs in train stations, the sector needs to balance scalability with the local, human touch that shapes Europe’s grocery culture.

Europe Online Grocery Market Segmentation:

The report segments the market based on product type, distribution channel, and region:

Study Period:

Base Year: 2024

Historical Year: 2019-2024

Forecast Year: 2025-2033

Analysis by Product Type:

-

Vegetables and Fruits

-

Dairy Products

-

Staples and Cooking Essentials

-

Snacks

-

Meat and Seafood

-

Others

Analysis by Business Model:

-

Pure Marketplace

-

Hybrid Marketplace

-

Others

Analysis by Platform:

-

Web-Based

-

App-Based

Analysis by Purchase Type:

-

One-Time

-

Subscription

Country Analysis:

-

Germany

-

France

-

United Kingdom

-

Italy

-

Spain

-

Others

Competitive Landscape:

The market research report offers an in-depth analysis of the competitive landscape, covering market structure, key player positioning, top winning strategies, a competitive dashboard, and a company evaluation quadrant. Additionally, detailed profiles of all major companies are included.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145